UX case study

Digital Verification System

Leading the end-to-end design of a first-in-industry pilot to integrate digital identity verification into retail banking. Partnering with Mitek Systems to validate the technology, user experience, and branch adoption across 3 pods at TD Bank.

Role

Lead UX Designer

Client

TD Bank

Platform

Omni-channel

Scope

3 Pods, Cross-platform

Project Overview

TD Bank set out to become the first retail bank in the industry to integrate digital identity verification directly into the in-branch experience. This was a pilot initiative, not just a product launch, designed to test whether digital verification could realistically replace manual ID review in a high-stakes retail banking environment.

The pilot had three distinct goals: validate the technology (through a partnership with Mitek Systems), validate the user experience for both colleagues and customers, and validate branch adoption at scale.

The challenge was especially complex given the variety of identification documents from various countries, the varying quality of physical IDs, and the high-stakes environment of in-branch account opening, all while proving a new third-party technology could meet TD's standards.

A First-in-Industry Pilot:

Three things to validate

Technology

Could Mitek's verification engine handle real-world ID variety and quality at the speed retail banking demands?

Adoption

Would branch colleagues actually choose this new flow over their familiar manual workflow?

Experience

Would the colleague and customer flows feel intuitive enough to outperform the legacy manual process?

My Role & Approach

As the lead UX designer, I owned the end-to-end experience design, from the colleague triggering DVS on their screens, to the customer receiving and completing verification on their phone, back to the colleague continuing the onboarding process once verification was confirmed.

End-to-End Experience Design

Defined the complete user journey across both the colleague-facing screen experience and the customer-facing mobile verification, ensuring seamless handoffs between the two.

Cross-Pod Coordination

Coordinated design across three separate pods. Aligning designers, developers, product owners, and BSAs so each team understood the big picture while delivering within their scope.

Stakeholder Advocacy

Presented the colleague-facing design to business partners, articulating design rationale and securing buy-in on key decisions that shaped the final experience.

This flow map was the single source of truth I maintained to keep all three pods aligned on the end-to-end experience — from the colleague initiating DVS through customer verification and back to onboarding.

The Challenge

TD Bank's branch colleagues manually verified customer IDs during account opening — a process that was slow, inconsistent, and vulnerable to fraud. With 1,100+ branches processing thousands of new accounts monthly, the manual approach couldn't scale. Colleagues had no standardized way to validate IDs, leading to inconsistent decisions and increased fraud risk.

Problem Statement

"How might we make it easier for colleagues to ID proof our customers in the branch, making everyone feel more confident and safe?"

Process Transformation

Before: Manual Review

Colleagues visually inspected physical IDs, relying on personal judgment.

Inconsistent validation standards across 1,100+ branches.

No permanent digital record of the ID for future compliance audits.

High vulnerability to sophisticated fraudulent documents.

After: Digital Verification

Digital scanning and facial recognition handle the heavy lifting.

Standardized, system-driven pass/fail decisions.

Permanent digital ID records stored securely for compliance.

Automated verification drastically reduces fraud risk.

Research & Discovery

Comprehensive

Competitive analysis of existing verification solutions in the market.

5

Key themes identified from in-depth interviews with branch colleagues and store managers

Colleague Insights: 5 Key Themes

Efficient Technology

Store managers imagined a simple experience, similar to the DMV. Colleagues take a picture, scan the ID, and the system does the rest.

Trigger DVS Early

Store managers expressed a need to have DVS done early in the process so they don't waste time on other pieces of account opening.

Process Consistency

Colleagues want to know what goes into a pass/fail decision and the factors that determine if an ID qualifies as legitimate.

Store IDs & Attestations

An added benefit of DVS is storing the ID on the customer profile permanently for future compliance records.

Consider Edge Cases

We need to consider what kinds of documents work with the solution, including non-resident aliens (NRAs) or minors.

Key Design Decisions

Trigger DVS Early

Informed by: Trigger DVS Early & Efficient Technology

Research showed colleagues wasted time on later steps when IDs failed. Moving verification to the start of onboarding saved time and reduced frustration.

Leverage Existing Flow

Informed by: Process Consistency

Another team had already designed the customer-facing DVS experience. We focused strictly on the colleague side, ensuring seamless handoff between the two experiences.

Design for Edge Cases

Informed by: Consider Edge Cases & Store IDs

We accounted for multiple document types, non-resident aliens requiring multiple IDs, and minor account openings — ensuring the system handled real-world complexity.

Design Evolution

The colleague flow went through multiple iterations. We explored different ways to initiate the verification—from QR codes to SMS links—and refined the waiting states based on feedback from branch testing.

Each row below represents a design iteration. From top to bottom: initial proposal → MVP1 happy path → QR code variant → SMS with progress tracker → loading overlay refinements → post-feedback updates incorporating stakeholder and colleague input.

Initial Proposal

Exploring the happy path and basic integration with the existing prospect creator flow.

Trigger Variations

Testing different initiation methods including QR code scanning vs. SMS text links.

Refining the Wait State

Adding progress trackers and loading overlays to keep colleagues informed while the customer completes their steps.

Final Colleague Experience

The final banker-facing flow prioritizes clarity and minimal interaction, allowing the colleague to focus on the customer in front of them.

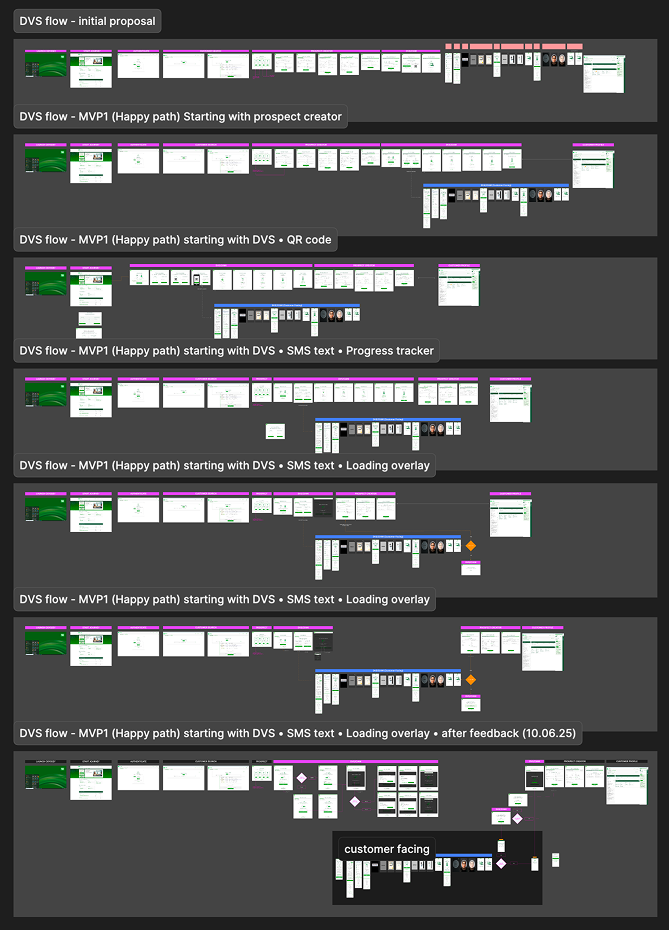

Initiate Verification

Colleague enters the customer's phone number to send a secure SMS link, triggering the process.

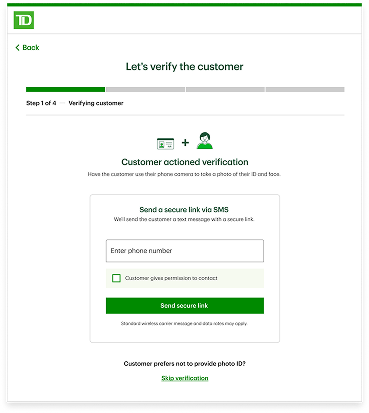

Processing State

A clear loading state informs the colleague that the secure link was sent and provides a resend option if needed.

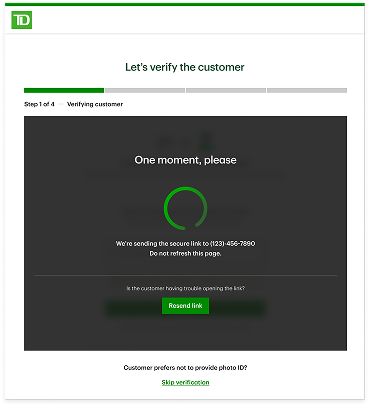

Verification Complete

Unambiguous success confirmation allows the colleague to confidently continue the account opening process.

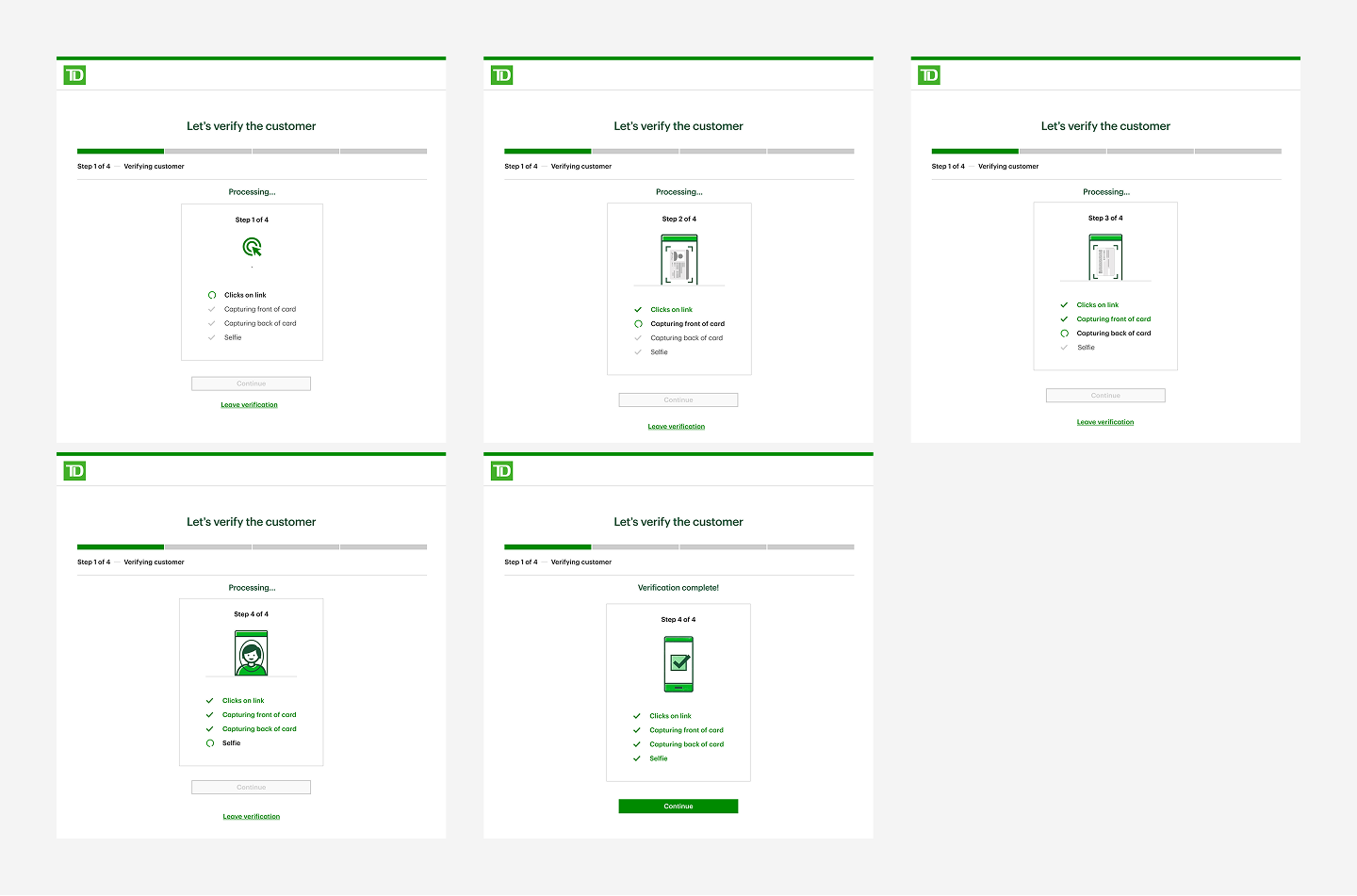

Customer Verification Flow

While the colleague waits, the customer completes a secure, step-by-step verification process on their own device, capturing their ID and a selfie.

Pilot Outcomes

Results & Impact

The pilot validated all three goals — proving the Mitek technology, the experience design, and branch adoption could work together at retail scale.

~3 min

Verification time (down from ~15m)

40

Branches with standardized process

100%

Digital ID records for compliance

Positive

Colleague feedback in testing

Learnings & Reflections

Design for the physical environment. Designing for branch colleagues requires understanding their physical context — they're standing at a desk interacting with a customer, not sitting alone at a computer. The UI needed to be highly scannable and require minimal interaction.

Edge cases aren't edge cases when they happen daily. Non-resident aliens and minors opening accounts are common enough to be core flows, not afterthoughts. Building the system to handle this complexity from day one was crucial for adoption.

Cross-pod alignment requires a shared artifact. With three pods working on different pieces of the same journey, misalignment was the biggest risk. Maintaining a single end-to-end flow map as the source of truth — and walking each team through it regularly — was what kept the experience cohesive. Next time, I'd establish that shared artifact even earlier in the process.